Nov 2016

30

New Proposed Statutory Payment Rates Announced for 2017-18

For the new tax year 2017-18, the Department for Work and Pensions have published the proposed statutory payment rates for benefits and pensions. The recovery amounts have not been published yet. Here is a link to the full list published - https://www.gov.uk/government/publications/proposed-benefit-and-pension-rates-2017-to-2018.

Please see some rates details below:

| 2016-17 | 2017-18 | |

| SAP, SMP, SPP, SSPP | ||

| Earnings threshold | £112.00 | £113.00 |

| Standard Rate | £139.58 | £140.98 |

| SSP | ||

| Earnings threshold | £112.00 | £113.00 |

| Standard Rate | £88.45 | £89.35 |

Nov 2016

16

Huge increase in The Pension Regulator's fines for Non-Compliance

The Pension Regulator's quarter figures for 1st July to 30th September 2016 have been released and there has been a huge rise in the number of notices and penalties issued to employers for non-compliance with auto-enrolment.

In this quarter The Pension Regulator issued 15,073 compliance notices, an increase of over 344% from the last quarter with 3,392 being issued. 3,728 fixed penalty notices carrying fines of £400 were also issued, an increase of 861 from the last quarter, up by 30%. Between July and September The Pension Regulator also issued 576 escalating penalty notices, up from 38 in the previous quarter. Depending on the size of the employer, these escalating penalty notices can carry a daily fine ranging between £50 and £10,000 per day.

The Pensions Regulator (TPR) says the rise is in line with the sharp increase in employers reaching their deadline to comply with auto-enrolment duties.

Since auto-enrolment was introduced in 2012 the following have been issued:

• 741 escalating penalty notices

• 26,040 compliance notices

• 6,779 fixed penalty notices.

A regulator spokesperson said: “Although the vast majority of employers are successful in meeting their duties, the minority of employers who fail to listen to warnings from us are subject to fines.”

The latest compliance and enforcement bulletin also emphasizes that explanations given by employers for non-compliance such as illness, being short staffed or confusion about their duties or miscommunication between employers and their advisers/agents are not a “reasonable excuse”.

Nov 2016

11

Making Tax Digital – How agents can prepare their business

Our good friends and tax software specialists, BTCSoftware, have been closely following the developments of HMRC’s Making Tax Digital programme. They have put together a handy overview which gives some background to the initiative, in particular Agent Services.

Agent Services encompasses the way accountants and tax advisers will be identified and authorised on HMRC’s systems to access client tax data and use other information facilities.

The guide is co-authored with accountingweb and also gives advice on how agents can prepare their practice and their clients for MTD’s arrival.

You can download a free copy here.

Nov 2016

7

New Living Wage Rates Announced

Annually, the first week in November is Living Wage Week and as part of this week, the new living wage rates details are revealed. The Mayor of London announces the London rate for the Living Wage whereas the UK rate is announced countrywide at the same time.

The new London Living Wage, announced by the Mayor of London, Sadiq Khan, has increased by 3.7%, from £9.40 to £9.75 per hour. This helps reflect the higher cost of living facing families in the city. The UK Living Wage rate has increased by 20p from £8.25 to £8.45, an increase of 2.4%. The Government's current minimum wage for over 25s is £7.20, which is £1.25 less than this rate.

There are nearly 1000 London-based employers that have agreed to pay their staff the Living Wage hourly rate, this is an increase of 300 employers. In total nearly 1,000 employers have signed up since Living Wage Week last year bringing the total number of accredited Living Wage organisations to nearly 3000. New companies that have signed up are RSA Insurance Group, Curzon Cinemas, the British Library.

For information about the Living Wage Foundation and Living Wage week visit the Living Wage Foundation website

- See more at: https://www.cipp.org.uk/news-publications/news/voluntary-living-wage-rates-announced.html#sthash.3zt9o68v.dpuf

Nov 2016

2

After Auto Enrolment Staging - What happens next??

Once you have completed the initial setup of auto enrolment you will need to complete a set of tasks on an ongoing basis. Clients will need to comply with their ongoing duties to avoid being fined by the Pensions Regulator.

Ongoing Assessment: All employees must be monitored on an ongoing basis to see if there are any changes to their worker category. For example, if an employee turns 22 or their qualifying earnings increase then they may become an eligible jobholder. Even if this occurs after staging, your client will still need to carry out new AE assessment duties for this individual employee.

Your payroll software should easily monitor the ages and earnings of any new and existing staff. Good payroll will automatically notify you of any changes to an employee's status therefore there should be no need to run a report every pay period. Any employees that become eligible will need to be enrolled and an AE communication letter issued to them.

Record Keeping: Clients must keep records of their auto enrolment activities for six years. They must also keep any employee opt-out notices for a period of four years. By law, there are two different types of records that an client must keep.

- Pension staff records- including employees names and addresses that have been enrolled, records of when the contributions were paid to the pension scheme, any opt-out notices and much more.

- Pension Scheme records - including the client pension scheme reference and scheme name and address.

These records or reports should be available in your payroll software

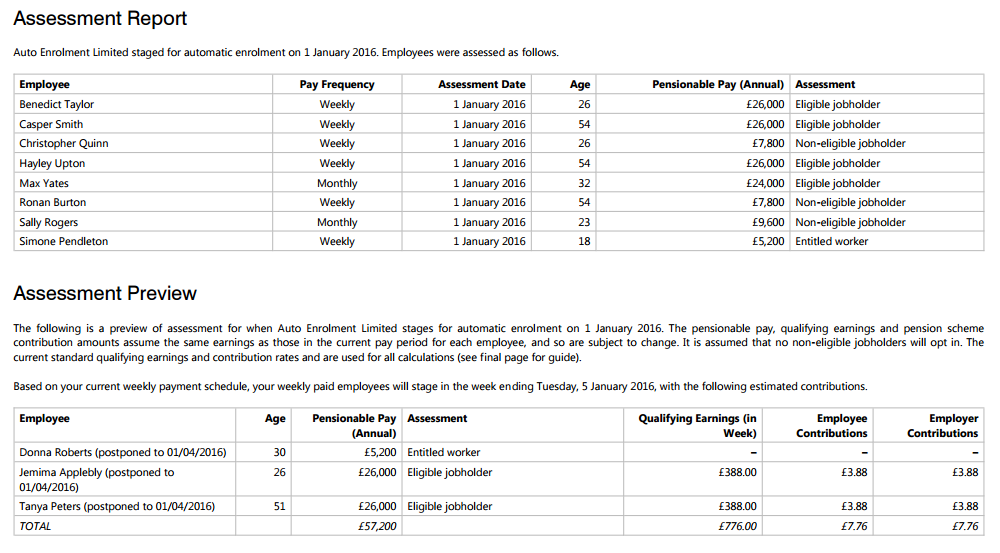

Post Assessment Report: A useful report to run is a post assessment report after your client has staged. The report will give your client a clear picture of what has taken place on the staging date for each employee. Your payroll software should easily produce this report to include each employee, pay frequency, assessment date, employee’s age, pensionable pay and assessment category. It would also be valuable to see employees who have been postponed. PDF Example post assessment report.

Pension Submission: Your payroll software should work and support your auto enrolment pension scheme. Each pension provider requires their data files in a certain format. Check to see if your payroll allows for the easy transfer of data files to the pension scheme. Some providers such as NEST and Smart Pension offer a direct integration or an API facility between payroll and pension provider which will save you time each pay period. Read: How useful will the NEST API tool be?

Paying Contributions: Your client will need to pay the correct level of employee and employer contributions to the AE pension scheme in a timely fashion. The contribution amounts will either be based on a fixed amount or a percentage of earnings. You payroll software should easily calculate both fixed or percentage amounts for you. One you have set up the contribution calculation basis then you payroll should deduct the correct amounts automatically for you.

To conclude..

The responsibility for meeting your automatic enrolment duties ultimately lies with your client. However if you are contracted to carry out AE on behalf of your client then you have an obligation to fulfill the terms of the contract. View a full list of Auto Enrolment Features in BrightPay.

25% BrightPay when you Switch!!

New bureau customers can now save 25% when they switch to BrightPay. To avail of the discount, you can purchase online or contact our sales team on 0845 3004 304 or sales@brightpay.co.uk and quote '25% Discount Sale'.

*Offer applies to new bureau customers who switch from a different payroll software provider for the first year subscription only. Applies to BrightPay 16/17 bureau licences only.