Scottish Rate of Income Tax (SRIT)

The Scottish Rate of Income Tax came into effect on 6 April 2016.

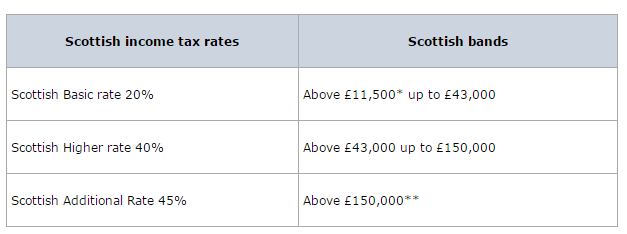

Scottish rates and bands for 2017/18

On the 21 February the Scottish Parliament voted to to freeze the basic rate of income tax of 20 per cent, also freeze the higher and additional rates at 40 per cent and 45 per cent respectively, and maintain the higher rate of income tax threshold at £43,000 in 2017/18, as set out in the table below.

HM Revenue and Customs (HMRC) will collect the Scottish rate of Income Tax on behalf of the Scottish government.

Who will pay the Scottish Rate?

HM Revenue and Customs (HMRC) will identify who will be a Scottish taxpayer and will issue new tax codes which will begin with the letter 'S'. Employers and pension providers don’t need to decide this and should only use a Scottish tax code if HMRC tell them to.

Employees will be classed as a Scottish taxpayer if the address HMRC holds for them is in Scotland. It is the employee's responsibility (not the employer) to notify HMRC if their address has changed, or which home counts as their main home if they have one in Scotland and one somewhere else in the UK.

If an employee disagrees with their tax code, they are advised to read the guidance on the Scottish rate of Income Tax before contacting HMRC.

Employer Duties

Employers won’t need to change how they report or make payments for Income Tax to HMRC, other than to apply the Scottish rate of Income Tax code to their Scottish taxpayer employees.

Employers must still apply the Scottish tax code for a Scottish taxpayer even though, overall, the amount of tax they pay isn’t changing.

If you are given a P45 with a Scottish tax code, follow the normal procedure. Week 1/ Month 1 basis will also apply to Scottish tax codes. If a new starter doesn’t provide a P45 and you are unsure which tax code to use, use the rest of the UK tax code and rate. HMRC will subsequently tell you if you need to change the tax code.

Employers won’t need to show the Scottish rate separately on employees' P60s or payslips, but should show the Scottish tax code.

Need help? Support is available at 0345 9390019 or [email protected].