Off-Payroll Working (IR35)

What is IR35?

In 2000, HMRC introduced IR35 (or the ‘off-payroll working rules’) to tackle what they call ‘disguised’ employment, i.e. individuals working through their own company, who would be employed if engaged directly, therefore having the right to all the tax breaks that those working under limited companies receive.

Unfortunately, the legislation in its original form was unenforceable, and in April 2017, the government introduced the ‘Off-Payroll Reforms’ to tackle non-compliance in the public sector. This shifted the responsibility for determining employment status from the individual working through the intermediary to the public authorities engaging them. The client, or public sector body, is also required to pay employment taxes on top of the fees paid to the contractor.

April 2021 Changes for the Private Sector

From April 2021, the rules change for contractors working with medium to large sized clients in the private sector. Like the public sector, clients must determine whether the contractor falls inside or outside IR35, deduct the right tax and National Insurance contributions and remit this directly to HMRC on behalf of the worker, through RTI.

Essentially, an organisation who takes on contractors is now responsible for deciding whether the rules should apply and making sure they and their workers pay the right tax. CEST (Check Employment Status for Tax), which is HMRC’s online tool, helps determine whether a contractor is inside IR35.

If you’re a contractor and you’re ‘inside IR35’, your client (being the public sector company or large/medium sized private company) must treat you as an employee and must apply income tax and National Insurance, just as they do for regular employees.

If you are inside IR35, you the individual becomes an employee of the deemed employer even though you may be acting through an intermediary e.g. your own limited company. You may still remain employed by your intermediary, but any salary from this intermediary will now be exempt from employment taxes as these have already been deducted and paid by your client. The rules do not entitle you to employment rights in respect of your work for the client. Instead, they make sure that workers, who would have been an employee if they were providing their services directly to the client, pay broadly the same tax and National Insurance contributions as employees.

What are off-payroll workers not entitled to?

Off-payroll workers are not entitled to receive or have deducted from their pay:

- Statutory payments: SSP, SMP, SAP, SPP, ShPP or SPBP

- National Minimum Wage / National Living Wage rates

- Annual leave entitlement / holiday pay

- Student Loans or Postgraduate Loans

- Automatic enrolment pension scheme contributions

Setting up an Off-Payroll Worker in BrightPay

- Set up a new record for your off-payroll worker in the same way you would for a new employee by selecting Employees > New Employee

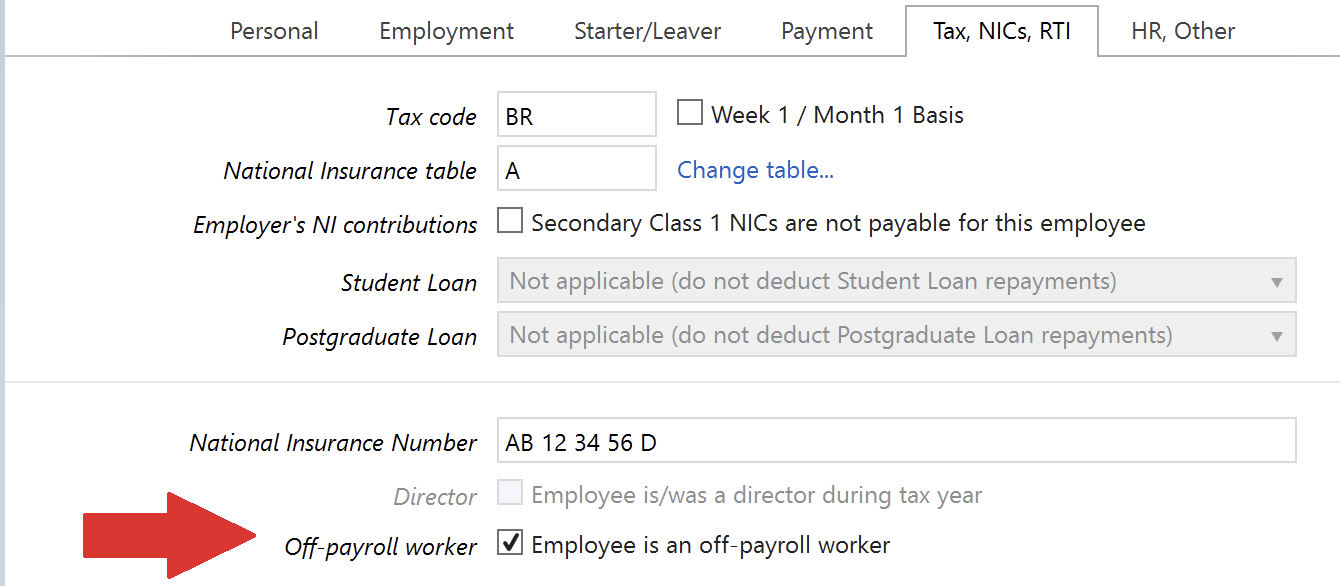

- Within the Tax,NICs,RTI section of the employee record, simply tick to indicate that the employee is 'an off-payroll worker':

- Save the employee record.

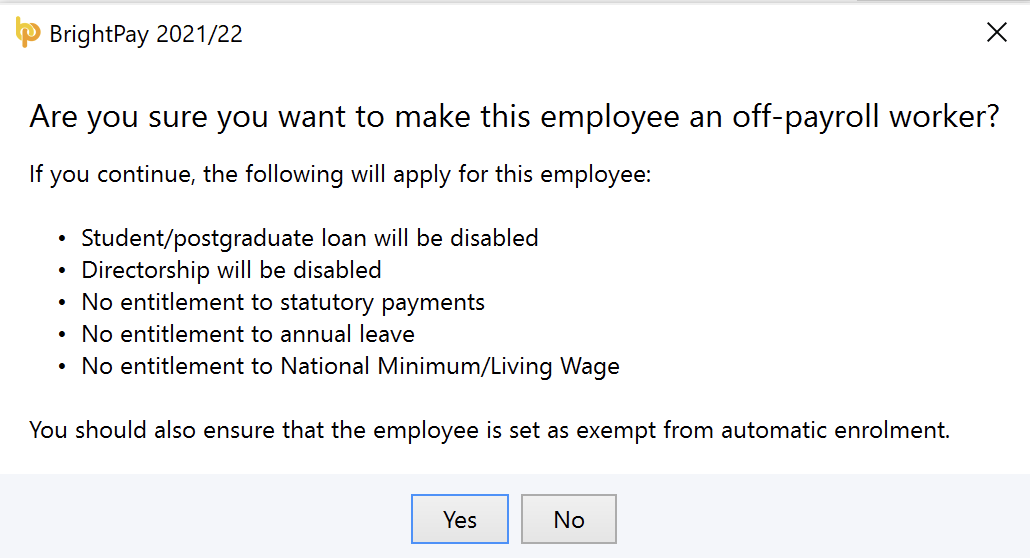

Once an employee is set up in BrightPay as an off-payroll worker, some settings will be automatically disabled. The settings that will be automatically disabled are:

- student & postgraduate loans

- directorship

- annual leave entitlements.

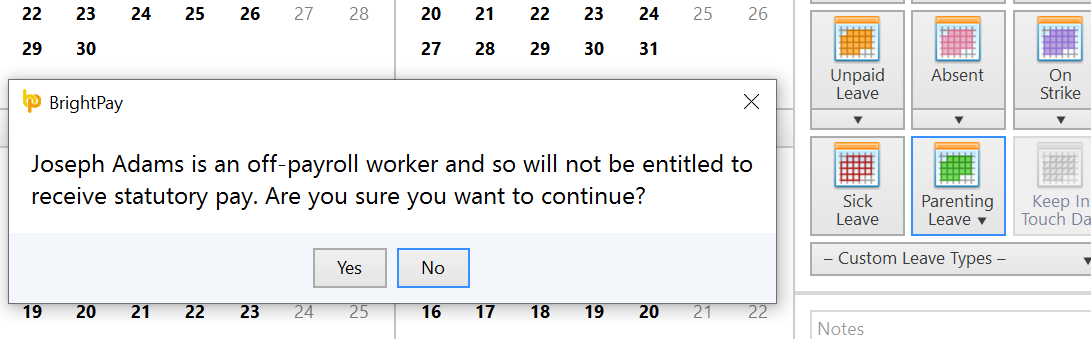

Should you subsequently add statutory leave for the off-payroll worker, a notification will highlight that the worker is not entitled to statutory pay, and the payment will not flow through to the payroll. However, the calendar can still be used should you wish to track this information internally.

For automatic enrolment, an alert will appear for the off-payroll worker in the Payroll utility. Simply mark them as being exempt from auto enrolment.

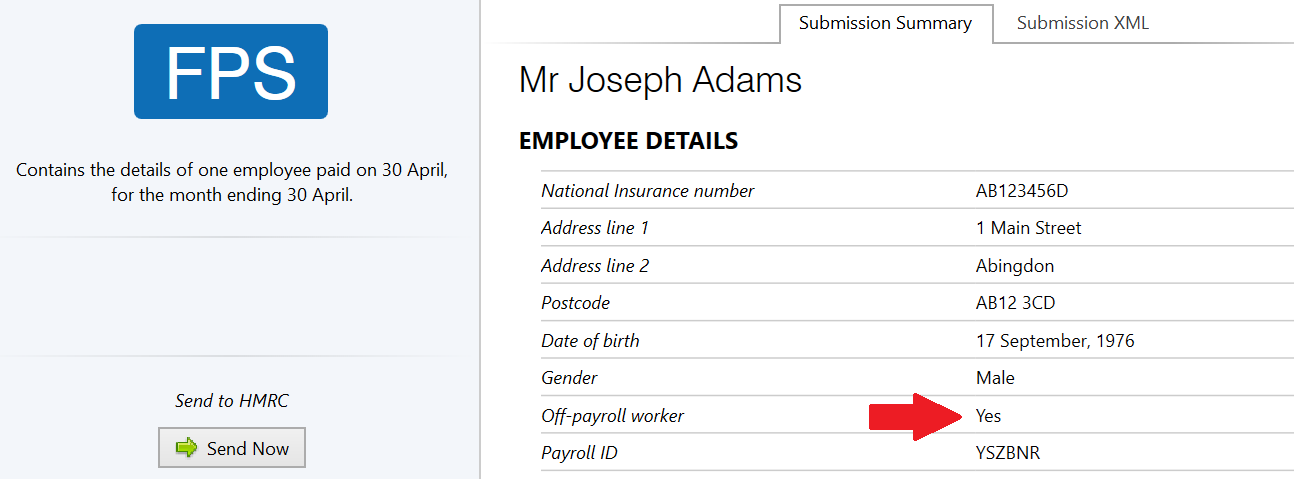

Each relevant Full Payment Submission will subsequently notify HMRC of any workers who fall inside IR35:

Considerations for a Contractor who has been deemed to be inside IR35

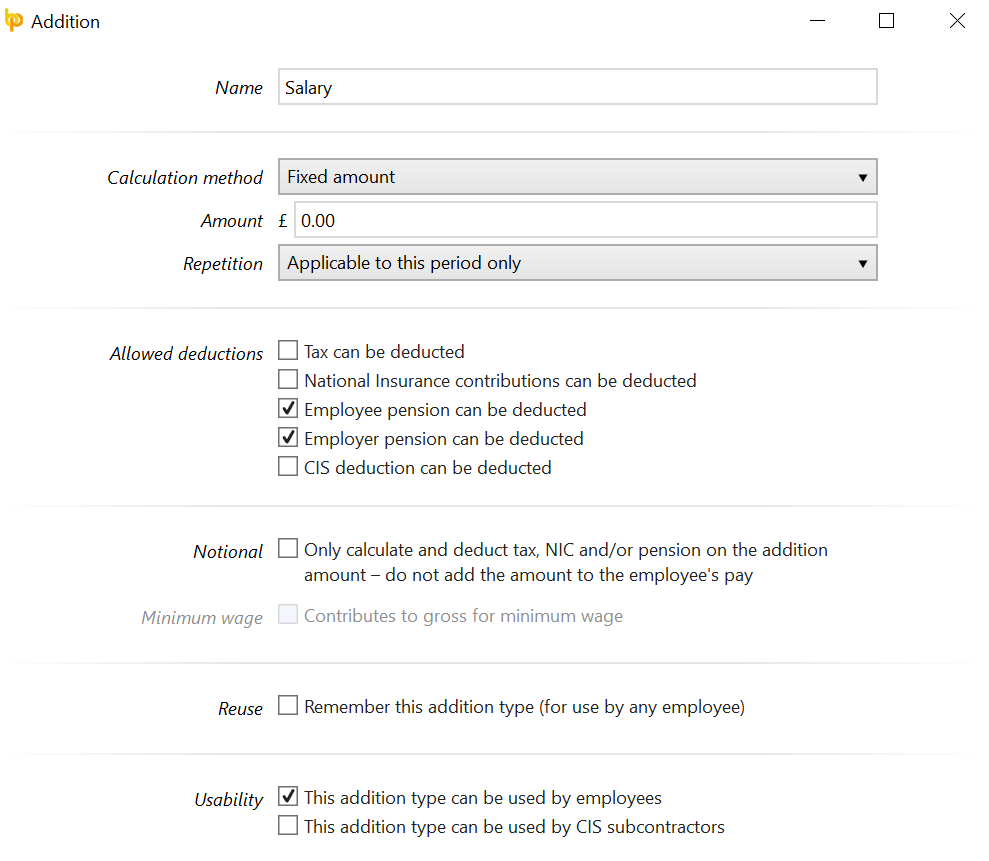

Salaries paid to you by your own limited company can be paid without deduction of PAYE and NIC. This is because payroll taxes have already been suffered on the payments from your client.

To achieve this, add a new addition type, give it a name (e.g. Salary) and untick the boxes ‘Tax can be deducted’ and ‘National Insurance contributions can be deducted’.

Need help? Support is available at 0345 9390019 or [email protected].