NIC Category Letters

Employers use an employee’s National Insurance category letter when they run payroll to work out the contributions they both need to make.

Apprentices under 25 in qualifying circumstances

From April 2016, employers of apprentices under the age of 25 will no longer be required to pay secondary Class 1 (employer) National Insurance contributions (NICs) on earnings up to the Upper Earnings Limit (UEL), for those employees.

Such apprentices must be following an approved UK government statutory apprenticeship framework (frameworks can differ depending on the UK country).

A new NI category 'H' is to be used for apprentices under 25 in qualifying circumstances.

Employer National Insurance Contributions for the Under 21s

Since 6 April 2015, employers are not required to pay Class 1 secondary NICs on earnings up to the ‘Upper Secondary Threshold’ (UST) - £827 per week, £3,583 per month - for employees who are under the age of 21. Class 1 secondary NICs will however continue to be payable on all earnings above the UST.

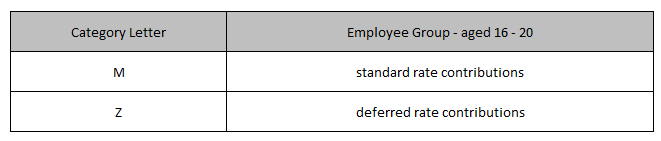

The following National Insurance Table Letters are applicable for under 21s:

Please note: if your employee is under 21 and meets the same conditions as an apprentice under 25, use NI category 'H'.

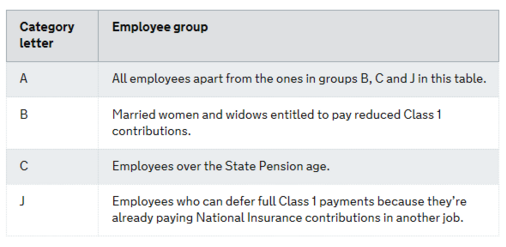

National Insurance Category Letters for Employees over the Age of 21

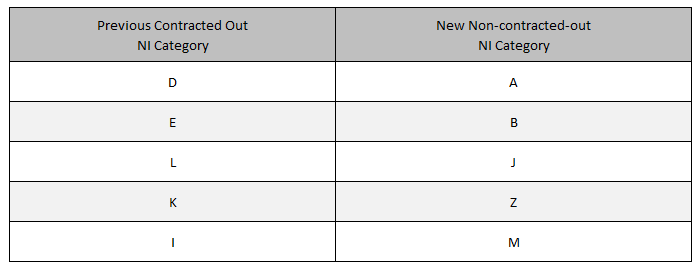

Abolition of Contracting Out

With the abolition of Contracting Out, HMRC have discontinued NI category letters D, E, K, I and L. Any employees in these categories in tax year 2015-16 will be given the equivalent non-contracting-out category.

Need help? Support is available at 0345 9390019 or [email protected].